USCPAリサーチ問題をサンプルテストで解く(FAR・AUD・REG)

どうやってリサーチ問題の対策をしたらいいのか分からなくて困ったな。

リサーチ問題は、AICPA提供のサンプルテスト(Sample Tests)を解いてみるといいと思うよ。

FAR、AUD、REGの3科目について、どんなリサーチ問題がサンプルテストに載っているか、一緒に見てみようね。

まだUSCPA(米国公認会計士)を目指してない場合

USCPAは受験資格を満たすのにUSCPA予備校のサポートがマスト。

どこがおすすめするUSCPA予備校はアビタスです。

\無料・すぐ読める・オンライン参加可/

どこの著書『USCPA(米国公認会計士)になりたいと思ったら読む本』も参考にしてくださいね。

USCPA資格の活かしかた・USCPA短期合格のコツを書いています。

(2026/07/08 09:35:17時点 Amazon調べ-詳細)

2024年1月以降の試験制度では、旧USCPA試験と同じ形式のリサーチ問題は出題されません。

新試験制度でのリサーチ問題は、課題を特定し、事実と添付された資料を検討・分析し、適切な対応を決定するものです。

リサーチ問題については、詳しくはこちらを参考にしてください。

サンプルテスト(例題)については、こちらを参考にしてください。

USCPA試験制度に関してのよくある質問(FAQ)は、こちらを参考にしてください。

USCPA試験に関するFAQ(よくある質問)を解説!受験生は確認マスト

音声で聞きたい人は、こちら。

USCPA試験FAQ(よくある質問)解説!学習ステージ別攻略法

1.FARのサンプルテストのリサーチ問題

FARのサンプルテストのリサーチ問題について見ていきましょう

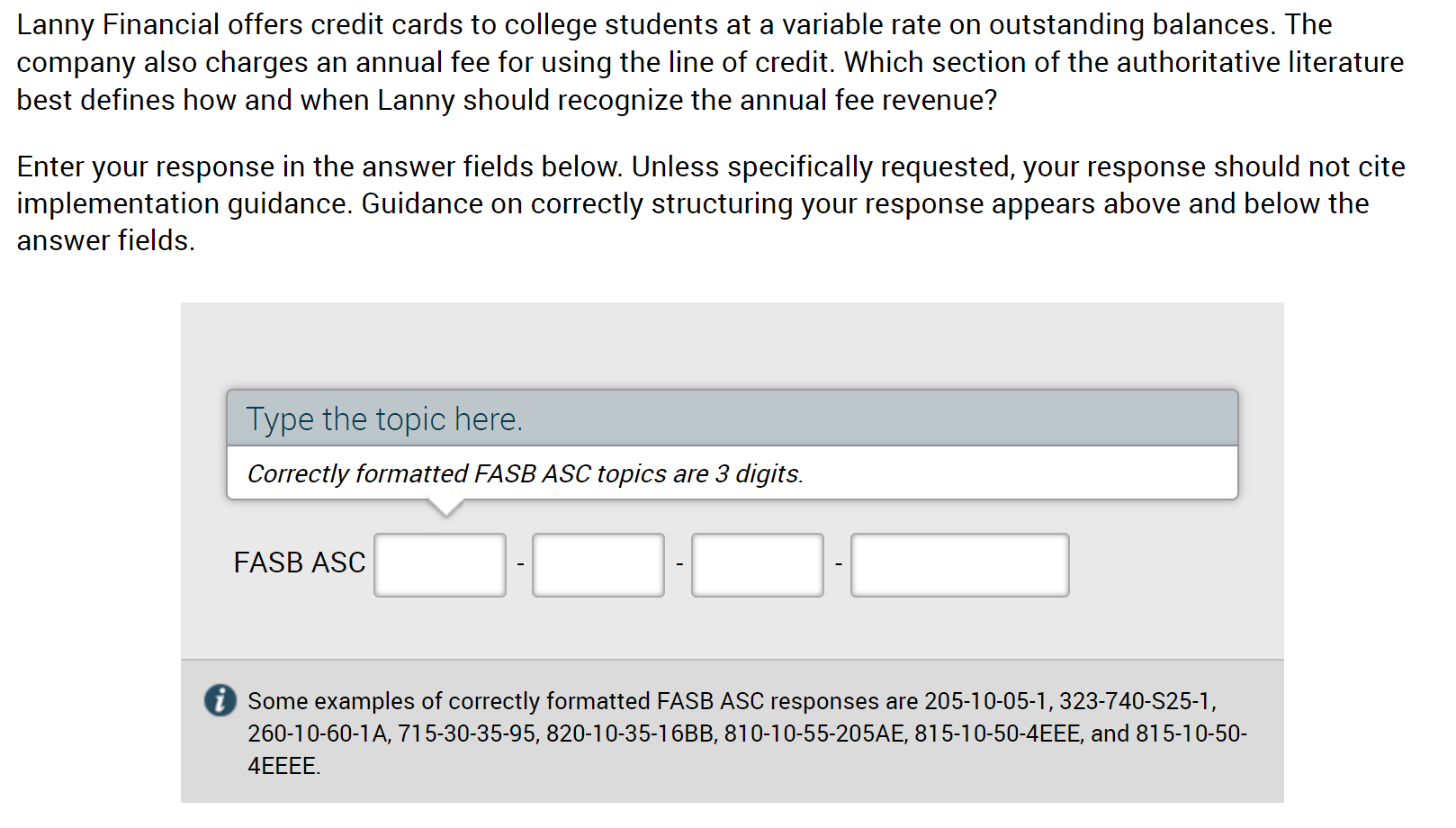

Lanny Financial offers credit cards to college students at a variable rate on outstanding balances. The company also charges an annual fee for using the line of credit. Which section of the authoritative literature best defines how and when Lanny should recognize the annual fee revenue?

Enter your response in the answer fields below. Unless specifically requested, your response should not cite implementation guidance. Guidance on correctly structuring your response appears above and below the answer fields.

(1)問題和訳

リサーチ問題の和訳は以下となります。

①シナリオ

- Lanny Financial社は、大学生を対象に、残高に応じた変動金利でクレジットカードを提供しています。

- また、同社は、与信枠の使用に対し年会費を徴収しています。

- 同社が年会費収入をいつ、どのように認識すべきかを最もよく定義しているのは、権威ある文献のどのセクションでしょうか?

②指示・補足

- 以下の解答欄に解答を入力してください。

- 特に要請がない限り、解答では適用指針を引用しないでください。

- 解答欄の上下には、解答を正しく構成するためのガイダンスが表示されています。

「適用指針を引用しない」などは、わざわざ記載されているので、従いましょう。

(2)解答

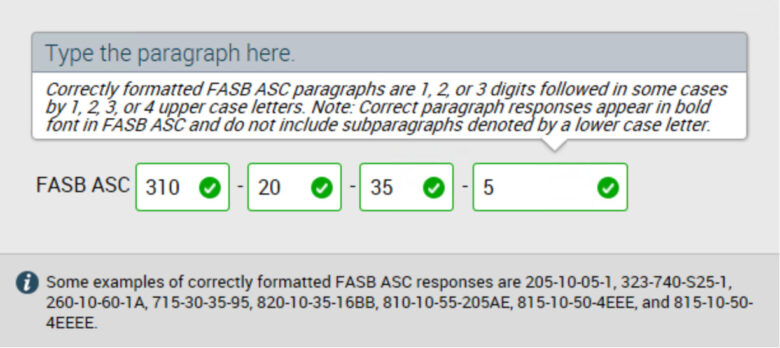

解答は以下となります。

FASB ASC 310 20 35 5です。

(3)解答補足

解答について補足をします。

①参照基準

FARのリサーチ問題では、FASB Codificationだけを参照します。

②参照先

FASB Codification

300番台:Assets(資産)

トピック:310 Receivables(売掛金)

サブトピック:20 Nonrefundable Fees and Other Costs(返金不可の料金とその他の費用)

セクション:35 Subsequent Measurement – General(後発測定 一般)

パラグラフ:5

③参照先の内容

トピック「310 Receivables(売掛金)」のサブトピック「20 Nonrefundable Fees and Other Costs(返金不可の料金とその他の費用)」のセクション「35 Subsequent Measurement – General(後発測定 一般)」のパラグラフ5の内容は、以下となります。

35-5Fees deferred in accordance with paragraph 310-20-25-15 shall be recognized on a straight-line basis over the period the fee entitles the cardholder to use the card. This accounting shall also apply to other similar card arrangements that involve an extension of credit by the card issuer.

35-5

310-20-25-15に従って繰り延べられた手数料は、カード所有者にカードを使用する権利を与える期間にわたって定額ベースで認識しなければなりません。

この会計処理は、カード発行会社による信用の拡大を伴う他の類似のカード契約にも適用されます。

FARのリサーチ問題で参照する基準に関しては、以下の記事を参考にしてください。

USCPA試験 FASB ASC (Accounting Standards Codification)の トピック 一覧

2.AUDのサンプルテストのリサーチ問題

AUDのサンプルテストのリサーチ問題について見ていきましょう。

注)2023年7月にサンプルテストのアップデートがあり、この問題は掲載がなくなりましたが、参考になるので役立ててください。

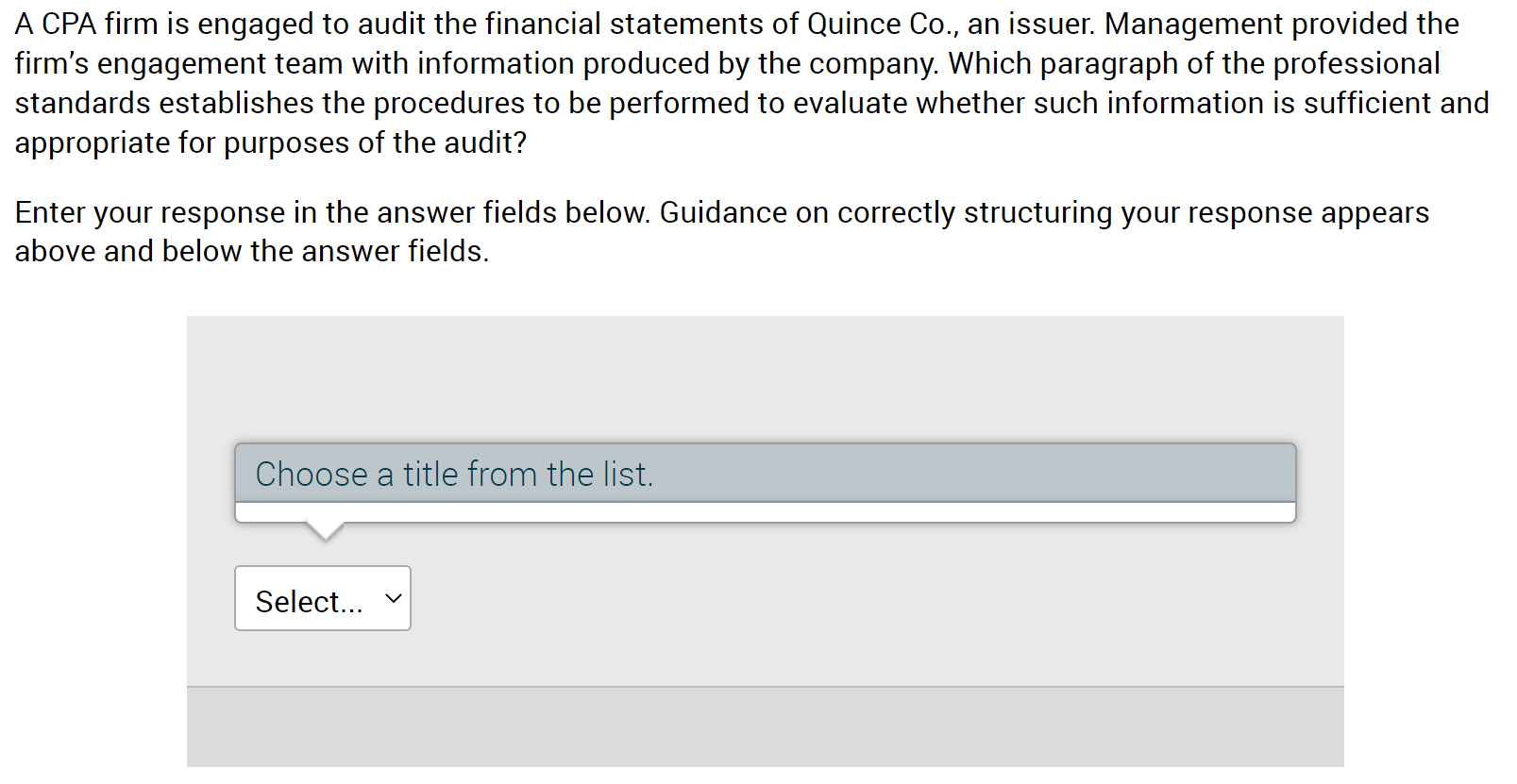

A CPA firm is engaged to audit the financial statements of Quince Co., an issuer. Management provided the firm’s engagement team with information produced by the company. Which paragraph of the professional standards establishes the procedures to be performed to evaluate whether such information is sufficient and appropriate for purposes of the audit?

Enter your response in the answer fields below. Guidance on correctly structuring your response appears above and below the answer fields.

(1)問題和訳

リサーチ問題の和訳は以下となります。

①シナリオ

- ある公認会計士事務所は、発行会社であるQuince株式会社の財務諸表の監査を請け負っています。

- 経営者は、会社が作成した情報を会社のエンゲージメントチームに提供しました。

- このような情報が監査の目的に照らして十分かつ適切であるかどうかを評価するために実施すべき手続を定めているのは、職業基準のどの段落ですか?

②指示・補足

- 以下の解答欄に解答を入力してください。

- 解答欄の上下には、解答を正しく構成するためのガイダンスが表示されています。

(2)解答

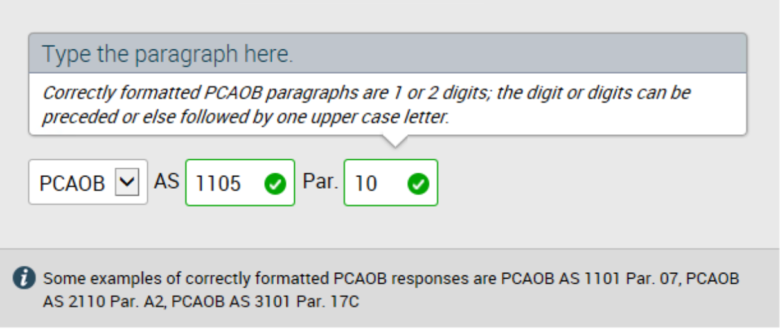

解答は以下となります。

PCOAB AS1105 Par.10です。

(3)解答補足

解答について補足をします。

①参照基準

シナリオに「an issuer(発行会社)」とあり、上場企業についての出題ですので、PCAOB Auditing Standards(PCAOB監査基準)を参照します。

②参照基準番号とパラグラフ

PCAOB Auditing Standards(PCAOB監査基準)

1000番台:General Auditing Standards(一般的な監査基準)

基準番号:AS1105 Audit Evidence(監査証拠)

パラグラフ:Par.10 Using Information Produced by the Company(会社が作成した情報の利用)

③参照先の内容

基準番号AS1105「Audit Evidence(監査証拠)」のパラグラフ10「Using Information Produced by the Company(会社が作成した情報の利用)」の内容は、以下となります。

Using Information Produced by the Company

.10 When using information produced by the company as audit evidence, the auditor should evaluate whether the information is sufficient and appropriate for purposes of the audit by performing procedures to:Test the accuracy and completeness of the information, or test the controls over the accuracy and completeness of that information; and

Evaluate whether the information is sufficiently precise and detailed for purposes of the audit.

会社が作成した情報の利用

10 企業が作成した情報を監査証拠として利用する場合、監査人は、以下の手続を実施することにより、当該情報が監査の目的に照らして十分かつ適切であるかどうかを評価しなければならない。

情報の正確性および完全性を検証するか、情報の正確性および完全性に関する統制を検証し、情報が監査の目的に照らして、十分に正確かつ詳細であるかどうかを評価する。

AUDのリサーチ問題で参照する基準に関しては、以下の記事を参考にしてください。

USCPA試験 AICPA Professional Standardsのセクション と PCAOB Auditing Standardsの基準番号 一覧

3.REGのサンプルテストのリサーチ問題

REGのサンプルテストのリサーチ問題について見ていきましょう。

注)2023年7月にサンプルテストのアップデートがあり、この問題は掲載がなくなりましたが、参考になるので役立ててください。

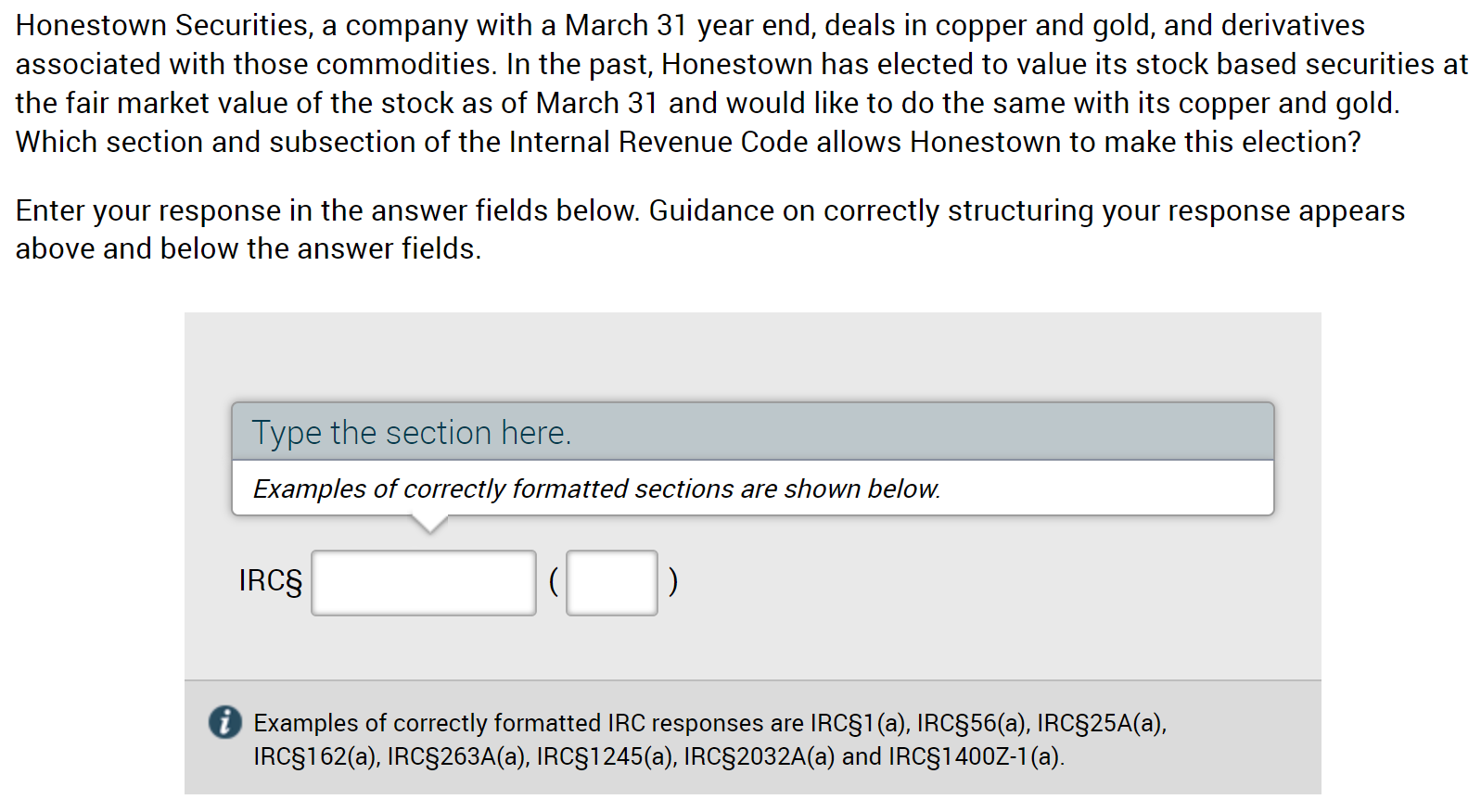

Honestown Securities, a company with a March 31 year end, deals in copper and gold, and derivatives associated with those commodities. In the past, Honestown has elected to value its stock based securities at the fair market value of the stock as of March 31 and would like to do the same with its copper and gold. Which section and subsection of the Internal Revenue Code allows Honestown to make this election?

Enter your response in the answer fields below. Guidance on correctly structuring your response appears above and below the answer fields.

(1)問題和訳

リサーチ問題の和訳は以下となります。

①シナリオ

- 3月31日決算のHonestown Securitiesは、銅と金、およびこれらの商品に関連するデリバティブを扱っています。

- これまでHonestownは、株式ベースの有価証券を3月31日時点の株式の公正な市場価値で評価することを選択してきましたが、銅と金についても同様にしたいと考えています。

- Honestownがこの選択を行うことができるのは、内国歳入法のどのセクションとサブセクションですか?

②指示・補足

- 以下の解答欄に解答を入力してください。

- 解答欄の上下には、解答を正しく構成するためのガイダンスが表示されています。

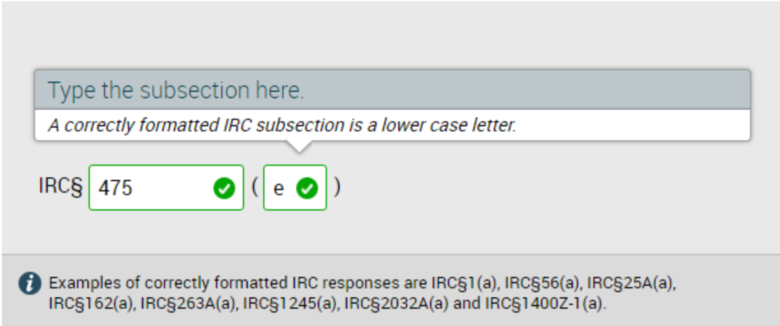

(2)解答

解答は以下となります。

IRC 475(e)です。

(3)解答補足

解答について補足をします。

①参照基準

REGのリサーチ問題では、Internal Revenue Codeだけを参照します。

②参照先

Internal Revenue Code

サブタイトル:A Income Taxes(所得税)

セクション:475 Mark to market accounting method for dealers in securities(有価証券のディーラーのためのMark to Market会計手法)

サブセクション:(e) ELECTION OF MARK TO MARKET FOR DEALERS IN COMMODITIES(コモディティのディーラーに対するMark to Marketの選択)

③参照先の内容

セクション「475 Mark to market accounting method for dealers in securities(有価証券のディーラーのためのMark to Market会計手法)」のサブセクション「(e) ELECTION OF MARK TO MARKET FOR DEALERS IN COMMODITIES(コモディティのディーラーに対するMark to Marketの選択)」の内容は、以下となります。

(e) Election of mark to market for dealers in commodities.

(1) In general. In the case of a dealer in commodities who elects the application of this subsection , this section shall apply to commodities held by such dealer in the same manner as this section applies to securities held by a dealer in securities.(2) Commodity. For purposes of this subsection and subsection (f) , the term “commodity” means—

(A) any commodity which is actively traded (within the meaning of section 1092(d)(1) );

(B) any notional principal contract with respect to any commodity described in subparagraph (A) ;

(C) any evidence of an interest in, or a derivative instrument in, any commodity described in subparagraph (A) or (B) , including any option, forward contract, futures contract, short position, and any similar instrument in such a commodity; and

(D) any position which—

(i) is not a commodity described in subparagraph (A) , (B) , or (C) ,

(ii) is a hedge with respect to such a commodity, and

(iii) is clearly identified in the taxpayer’s records as being described in this subparagraph before the close of the day on which it was acquired or entered into (or such other time as the Secretary may by regulations prescribe).

(3) Election. An election under this subsection may be made without the consent of the Secretary. Such an election, once made, shall apply to the taxable year for which made and all subsequent taxable years unless revoked with the consent of the Secretary.

(e) コモディティのディーラーに対するマーク・トゥー・マーケットの選択

(1)一般論として

本項の適用を選択した商品取引業者の場合、本項は、証券取引業者が保有する有価証券に本項が適用されるのと同じ方法で、当該業者が保有する商品に適用される。

(2)商品 本項および(f)項の目的上、「商品」という用語は以下を意味する。

(A)活発に取引されている商品(第1092条(d)(1)の意味内)。

(B)(A)号に記載された商品に関する想定元本契約。

(C)(A)号または(B)号に記載された商品の権利または派生商品の証拠(当該商品のオプション、先渡契約、先物契約、ショートポジション、および類似の商品を含む)。

(D)以下のようなポジション

(i)サブパラグラフ(A)、(B)、または(C)に記載された商品ではない。

(ii)そのような商品に関するヘッジである。

(iii) 取得または締結された日の終了前(または長官が規則で定める他の時間)に、納税者の記録で本項に記載されていることが明確に確認されている。

(3)選択

本項に基づく選択は、長官の同意を得ずに行うことができる。一旦選択された選択は、長官の同意により撤回されない限り、選択された課税年度およびその後のすべての課税年度に適用される。

REGのリサーチ問題で参照する基準に関しては、以下の記事を参考にしてください。

USCPA試験 Internal Revenue Code(内国歳入法) の内容一覧

以上、「USCPAリサーチ問題をサンプルテストで解く(FAR・AUD・REG)」でした。

あとは、USCPA予備校の演習問題を通して、検索の練習をしてみればいいね。

基準の内容をざっくり覚えておけば、あとは、どんなキーワードで探すかだけになるから、慣れるまで練習してみてね。

USCPA試験については、どこの著書『USCPA(米国公認会計士)になりたいと思ったら読む本』も参考にしてくださいね。

短期合格のコツも記載しています。

(2026/07/08 09:35:17時点 Amazon調べ-詳細)

まだUSCPAの学習を開始していない場合「USCPAの始めかた」も参考にしてください。